“[Credit is a system whereby] a person who can’t pay, gets another person who can’t pay, to guarantee that he can pay.”

― Charles Dickens

While Dickens humorously captures the perplexity of credit, in today’s real estate landscape, especially in the Puget Sound region, understanding the nuances of your credit score is vital if you’re considering buying a house through financing. Unless you are planning on buying your next house with cash you are going to want to know what makes your credit score go up and down.

The average price for a home in Snohomish County is $733,369 (NWMLS 12/19/23). The average price for a home in King County is $984,294 (NWMLS 12/19/23). This means if you are considering buying a house in a Puget Sound community you will probably need to make sure your credit is going up.

Your credit score influences your home buying potential. A good score can get you a lower interest rate and that will give you more buying power.

FICO® Credit Scores – Your Financial Barometer:

FICO® Scores are the credit scores used by 90% of top lenders to determine your credit risk. Credit scores range from 300 to 850, with 300 being the lowest and 850 being the highest.

Generally, the higher the credit score number the better the loan terms.

You have a credit score for each of the 3 major credit bureaus:

Your FICO® Scores are calculated using the information in your credit reports.

While you can get a credit score for free from many different websites and apps, most of these numbers do not reflect the actual credit score that your lender will see. Sites like, www.CreditKarma.com, are good for getting a good idea of how your credit looks but are not a substitute for contacting a bank or loan officer.

What Credit Score Do You Need To Get A Mortgage Loan?

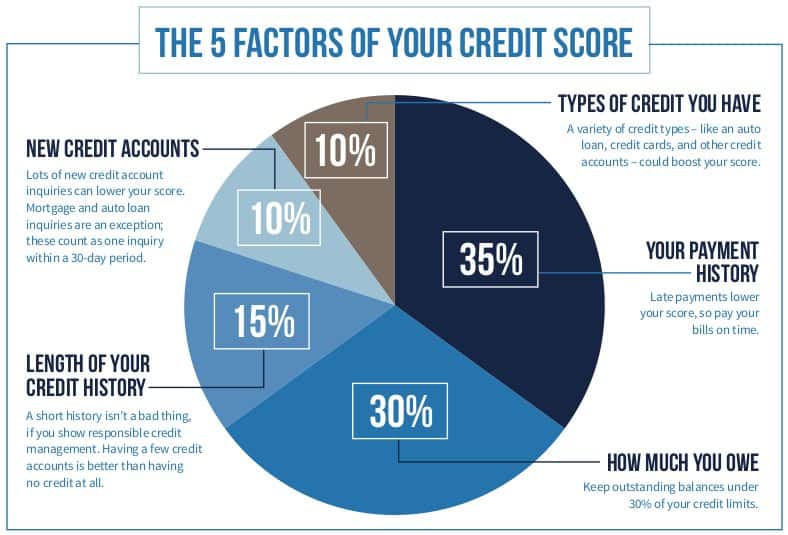

What Makes Your Credit Score Go Up and Down

1. Your Payment History – 35%

Late payments lower your score, so pay your bills on time

2. How Much You Owe – 30%

Keep your outstanding balances under 30% of your credit limits. Pay down your credit accounts to increase your score.

3. Length Of Your Credit History – 15%

A short history is not a bad thing if you show responsible credit management. Having a few credit accounts is better than having no credit at all.

4. New Credit Accounts – 10%

Lots of new credit account inquiries can lower your score. Mortgage and auto loan inquiries are an exception; these count as 1 inquiry within a 30 day period.

5. Types of Credit You Have – 10%

A variety of credit types — Like an auto loan, credit cards, and other credit accounts — could boost your score.

Immediate Actions To Increase Your Score

Check Your Credit Report

Credit score repair begins with your credit report. If you haven’t already, request a free copy of your credit report and check it for errors. Your credit report contains the data used to calculate your credit score and it may contain errors. In particular, check to make sure that there are no late payments incorrectly listed for any of your accounts and that the amounts owed for each of your open accounts is correct. If you find errors on any of your reports, dispute them with the credit bureau.Read more about Disputing Errors on Your Credit Report.

Setup Payment Reminders

Making your credit payments on time is one of the biggest contributing factors to your credit scores. Some banks offer payment reminders through their online banking portals that can send you an email or text message reminding you when a payment is due. You could also consider enrolling in automatic payments through your credit card and loan providers to have payments automatically debited from your bank account, but this only makes the minimum payment on your credit cards and does not help instill a sense of money management.

Reduce the Amount of Debt You Owe

This is easier said than done, but reducing the amount that you owe is going to be a far more satisfying achievement than improving your credit score. The first thing you need to do is stop using your credit cards. Use your credit report to make a list of all of your accounts and then go online or check recent statements to determine how much you owe on each account and what interest rate they are charging you. Come up with a payment plan that puts most of your available budget for debt payments towards the highest interest cards first, while maintaining minimum payments on your other accounts.

The Summary Of What Makes Your Credit Score Go Up and Down

In the Puget Sound area’s real estate market, your credit score is more than just a number; it’s a reflection of your financial health and a key determinant in your home-buying journey. Understanding how it fluctuates and what impacts it can be your stepping stone towards securing the home of your dreams.

So, start today, be consistent, and watch how these changes positively affect your score and, in turn, your home-buying potential in one of the most vibrant housing markets in the nation.

Share this post!

One Comment on “What Makes Your Credit Score Go Up And Down”

Great insights! I had no idea how much my payment history impacted my credit score. I’ll definitely be more mindful of my credit utilization moving forward. Thanks for the tips!